When the door closed on Wise in Pakistan, nobody said why. This investigation did not stop there.

By Samra The Correspondent | June 3, 2026

Umer works with multiple clients across the UK and the US.

He has a Wise account. It functions. The money moves.

But every time a new client asks for his Wise email, he cannot send one. He sends ACH details instead. A routing number. An account number. A manual bank transfer setup that takes longer and feels less professional than a simple payment link.

Every time he sends those details, the client hesitates.

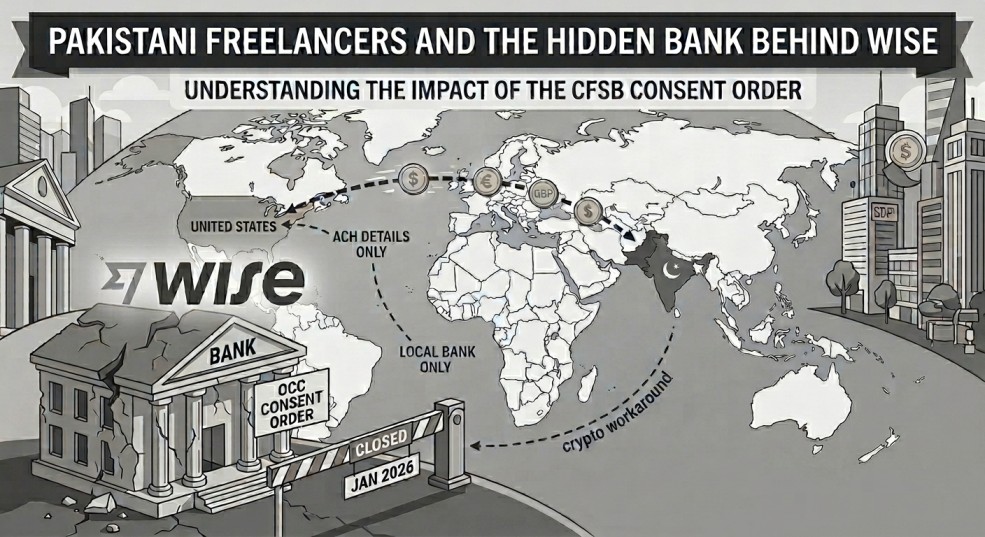

He has done nothing wrong. The platform has not failed him. He simply cannot register on Wise in Pakistan anymore. The door closed in January 2026. No public explanation was given.

Maheen’s situation is different. Her clients are in the US and the UK. They send her money via Wise directly to her local Pakistani bank account. She does not need a Wise account herself.

She thinks she is fine.

She does not know what is sitting underneath her clients’ Wise accounts.

Ashar uses iFast Global, Revolut, and Payoneer. Multiple platforms. Multiple workarounds. There is always a fear of accounts getting limited or banned. Most of his payments come through Upwork because it feels safer. But the fifteen percent fee plus weak conversion rates are another headache. A lot of freelancers he knows have started using crypto for direct clients. That is not a permanent solution either.

His words: most of us are just trying to manage with the options available until something permanent arrives.

Three people. Three different situations. One thing none of them know.

Wise is not a bank.

That sentence is the beginning of understanding everything that follows.

Wise is software. An interface. A brand built on top of banking infrastructure that most users have never heard of and were never told about.

The bank underneath Wise’s US dollar accounts is Community Federal Savings Bank, CFSB. A small savings institution at 89-16 Jamaica Avenue, Woodhaven, Queens, New York.

Wise’s own documentation confirms this. When a Wise account appears in an external payment system, it registers as Community Federal Savings Bank or CFSB. The routing number Wise assigns to US account holders belongs to CFSB. Every dollar a Wise user holds in a standard US account sits inside CFSB’s ledger.

Not Wise’s ledger. CFSB’s.

This week, Jason Mikula of Fintech Business Weekly confirmed in direct correspondence that the Wise-CFSB partnership remains active. Mikula has covered CFSB’s fintech partnerships since 2024 and is one of the most credible voices in global fintech journalism. He also noted that Wise has added Column Bank for some additional capabilities. The core CFSB relationship continues.

Maheen’s clients are routing money through CFSB right now. She does not know that bank exists.

CFSB is not a new story. That matters.

Fintech Business Weekly reported in September 2024 that CFSB grew from roughly 160 million dollars in assets in 2018 to nearly 860 million dollars by early 2024. A 438 percent jump built almost entirely on fintech partnerships.

Before that growth, CFSB had operated under OCC cease and desist orders from 2011 until 2022 for compliance failures. The moment those restrictions lifted, the bank leaned hard into banking as a service. It took on fintech programs including higher-risk ones that other banks had dropped after their own enforcement actions.

CFSB was the bank fintech programs went to when their previous banks got in trouble with regulators.

Pakistani freelancers were sending their income through it. Nobody told them.

On May 21, 2026, the Office of the Comptroller of the Currency issued a consent order against Community Federal Savings Bank. Docket AA-ENF-2025-21. Publicly available at occ.gov. This is not a rumor. It is a federal regulatory action, signed and dated.

The OCC’s findings are specific.

Since 2020, CFSB significantly grew its payment processing line, resulting in significant annual wire and ACH activity, including cross-border activity involving foreign financial institutions.

Despite that growth, CFSB failed to develop controls commensurate with the risks.

The finding that matters most: CFSB’s automated suspicious activity alerting system had deficiencies in its logic, data, and methodology. Those deficiencies caused the system to auto-close alerts that should have been escalated for further review. As a result, the system auto-closed a very high percentage of all ingested alerts.

A bank processing significant cross-border wire and ACH activity had built an automated compliance system that was quietly waving through transactions it was legally required to investigate. Not occasionally. At a very high percentage. For years.

That is the infrastructure underneath the platform Umer cannot register on. The platform Maheen’s clients use every day. The floor that was never disclosed to either of them.

Now the question nobody is asking.

Wise closed new registrations for users outside the United States in January 2026. Existing users like Maheen are still active. Wise confirmed this themselves: the pause does not impact customers with existing USD account details who can continue to use their accounts normally.

But CFSB is now under a federal consent order. That is not a fine and done. It is an ongoing corrective process. The OCC monitors compliance. Pressure does not ease after a consent order. It intensifies.

When pressure intensifies on a bank, the bank de-risks. When a bank de-risks, the platforms sitting on top of it follow. Wise has already shown exactly how that happens. New registrations outside the US closed quietly, with no public explanation, when CFSB’s risk appetite shifted.

If CFSB tightens further, existing accounts could follow.

Maheen would find out the way Umer did. A closed door. No explanation.

That is the pattern already in motion. Documented. On record.

Consider what Payoneer published in the three weeks before the consent order dropped.

April 30, 2026. Payoneer publishes Pakistan’s IT Exports: What’s Driving the Surge in 2026. The framing: Pakistan’s freelance ecosystem is maturing into structured B2B agencies. Payoneer positions itself as the reliable infrastructure needed for that scale. Institutional optimism. Published for Pakistani freelancers to read.

May 14, 2026. Payoneer and Upwork announce the extension of their fifteen-year partnership. The press release: seamless cross-border expansion. Reliable withdrawals. Faster access to international earnings.

May 19, 2026. Payoneer issues a second announcement aimed specifically at Pakistan. Same message. Same celebration. Directed at the exact freelancers whose infrastructure was under pressure.

May 21, 2026. The OCC publishes its consent order against Community Federal Savings Bank.

None of those three pieces of content mentioned CFSB.

None of them mentioned that Payoneer had been a CFSB partner for close to a decade, confirmed on record by CFSB itself in 2024.

None of them mentioned that Payoneer had since quietly moved its primary banking partner away from CFSB.

Wise has not moved. The Wise-CFSB relationship remains active today.

The freelancers being celebrated had no visibility into any of this.

Three weeks of institutional optimism. Then the federal regulator published what was actually happening inside the infrastructure.

This is the Sovereignty Gap moving upstream.

Pakistani freelancers are not operating inside a financial system. They are renting space on rails built by institutions that have no legal obligation to tell them anything.

That was one platform. One payment. One silence.

This is the same gap one level further up.

The gap is now between a freelancer in Islamabad and a compliance failure inside a federal savings bank in Queens that they have never heard of and were never told about. There is no Pakistani institution with authority over the OCC. There is no appeals process for a country restriction triggered by upstream regulatory pressure. There is no requirement that any platform tell you the name of the bank your income lives in.

CFSB grew to nearly a billion dollars in assets on the back of cross-border fintech partnerships. Pakistani freelancers contributed to that growth without knowing it. They were not told when it came under federal scrutiny. They were not consulted when the door closed.

They just stopped being able to register.

And Payoneer posted a celebration.

Ashar said it plainly: most of us are just trying to manage with the options available until something permanent arrives.

That sentence contains everything wrong with the current situation. A skilled professional, earning in dollars, serving clients across multiple countries, describing his financial life as something he is managing around while waiting for something permanent.

The platforms celebrating his earnings cannot tell him what bank his money lives in.

The regulators protecting that bank have no obligation to notify him when they act.

The Pakistani institutions mandated to protect him have no jurisdiction over any of it.

Two things would change this dynamic entirely.

When a platform restricts access for users in Pakistan, say why. One sentence. Public. That is all. Wise closed the door in January. It is May. Pakistani freelancers are still waiting.

When a platform’s banking infrastructure changes in a way that affects users, say so. The name of the bank underneath your account is not a trade secret. It should not take a federal consent order to find it.

Pakistani freelancers are earning close to a billion dollars a year. They deserve to know what infrastructure their income depends on.

That is not a complicated ask. It is the minimum.

—-

Sources

OCC Consent Order against Community Federal Savings Bank, Docket AA-ENF-2025-21, issued May 21, 2026. Publicly available at occ.gov.

Jason Mikula, Fintech Business Weekly. Direct correspondence, May 2026. Confirmed Wise-CFSB partnership active as of this week.

Fintech Business Weekly, September 2024. Reported CFSB fintech partnerships including Wise and Payoneer. CFSB confirmed both relationships on record at that time.

Wise official documentation confirming CFSB as banking partner. Publicly available at wise.com.

Payoneer-Upwork partnership announcement, May 14, 2026.

Direct correspondence with Umer, Maheen, and Ashar.

—–

Samra

The Correspondent